A sell-on-the-trumpets rally in gold following a firmer agreement of peace between Iran and the US and an opening of the Strait of Hormuz was cut short by the first press conference of the new Federal Reserve Chairman Kevin Warsh, who announced something of a re-writing of the rules at the Fed.

Spooked is probably too strong a word, but his pronouncement that the Fed’s forward guidance would be removed, that interest rates would remain where they are, and that potential overhauls of Fed communication, inflation frameworks, balance sheet control, and data sources would be forthcoming, led to an interruption in a broad market rally starting last Monday.

Yet the conference featured contradictions typical of past Fed language, and suggest that changes may not be as strong as Warsh seemed determined to convince reporters they’d be. His reassurance that the Fed will deliver price stability and acknowledgement that price inflation was too high, were words that belied actions of leaving interest rates where they were and of allowing the Fed’s balance sheet to expand another $11 billion.

Price stability itself is the promise that prices rise 2% every year, in other words—price inflation—albeit of a predictable sort. That in and of itself should be bullish for gold, but the language distorted the underlying facts and left traders believing that interest rate hikes were far more likely than cuts—a bearish sign for gold.

Axel Merk, founder and CEO of Merk Investments, argued in a recent interview that even if Warsh is serious about controlling inflation, it can take years to do so, as seen during the tenure of Paul Volcker, a previous Fed Chairman who raised interest rates substantially above the price inflation rate. Additionally, said Merk, less monetary policy uncertainty could have an unexpected benefit for gold, and if Warsh’s comments on removing forward guidance, projections, and dot plot estimations prove true, the fact that the market would be signaling to the Fed rather than the other way around would reduce volatility in gold and allow traders to focus on the true bull case: that fiscal deficits and government debt are too high to manage with policy the way it currently is.

A yippie yen

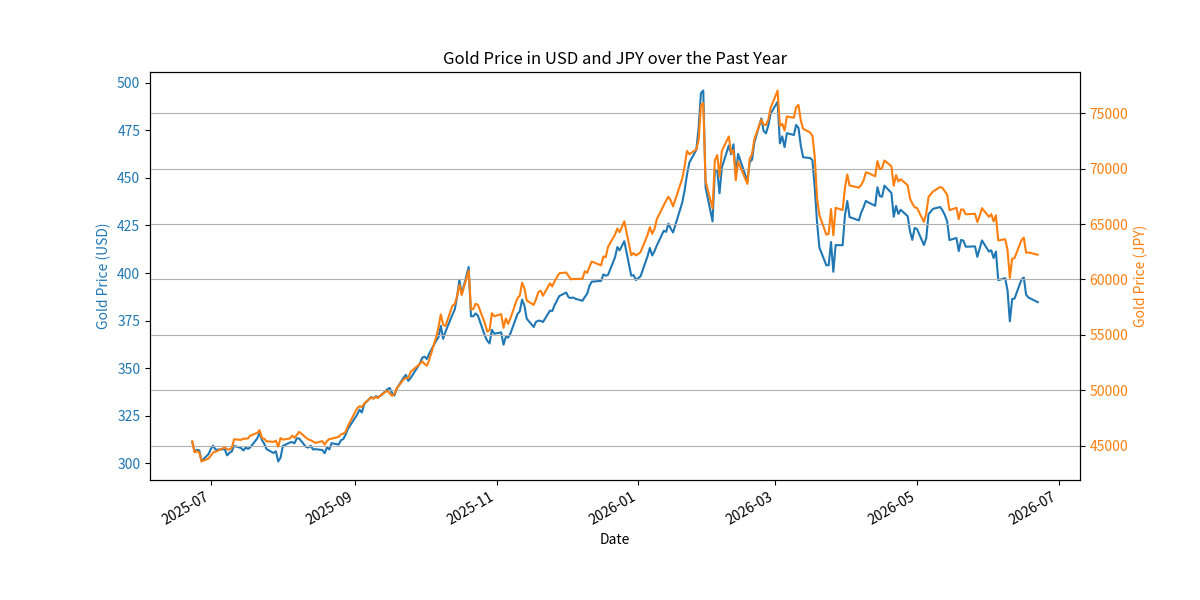

Gold lost much of what it had gained after rising from below $4,100 per ounce to above $4,300 on Wednesday. Bond yields fell (strengthened) on a stronger dollar, and the stronger dollar pushed the yen weaker.

The Japanese currency is wallowing in “intervention territory” as The Japan Times called it “as it crawled within a few tenths of a yen of a multidecade low”.

¥160 to the dollar is seen as a red line. ¥161.95 would mark the largest amount of yen per dollar since 1986. It currently stands at ¥161.75, and climbing above that would in practice demand of the central bank some kind of intervention. In May, the Bank of Japan expended some $35 billion in an effort to keep the currency from crossing this red line. Less than 2 months later it’s not only approached it again, but passed it.

Japan is the largest of US foreign creditors, holding over $1 trillion in US government debt which it could sell to support the yen. The BoJ recently rose interest rates to as high as 1% for the first time in decades.

On the surface, Japan has the largest debt burden of any nation with an economy worth mentioning—240% of GDP. Her net debt, however, is 130% of GDP. “The difference is financial assets, at least some of which can be sold in fairly short order, with the proceeds used to retire some of Japan’s debt overhang,” wrote Robin Brooks, Chief Forex Strategist at Goldman Sachs, on his Substack.

“Such a step would reduce the need for BoJ yield caps, stabilize the Yen and—most importantly—signal that Japan is finally getting serious about confronting its debt burden. The reason this hasn’t been done yet is that there’s vested interests that want to keep managing the various financial assets Japan’s government owns”.

How long that vested interest can anchor the government and BoJ’s inaction-action is debatable, but what isn’t is that such indecision benefits gold.

The premium for gold priced in yen steepens above the dollar as one measures back across the 9 month, 1 year, 3 years, and beyond. Investors have been perceiving the former as a greater risk than the latter. Decisive outflows of US bonds to retire Japanese debt would reverse not only the weakening trend in the yen, but weakness to the gold price as well. WaL

Consider Following the link here to see all the ways, monetary and non-monetary, you can support this work and more like it.

PICTURED ABOVE: Kevin Warsh at a Hoover Institution event, where he is a Distinguished Visiting Fellow. PC Hoover Institution, via a release.