Pierre Lassonde, the famous Canadian gold mining investor and executive, recently said in an interview that he believes gold could reach $17,200, a figure he generated by simply examining the historic ratio between the Dow Jones and gold.

His is just one of many high valuations that technical analysts and macro-investors will bandy about among the suite of media outlets that cover the gold market, but even JP Morgan Chase have their own price target of $6,000 per ounce for the yellow metal.

As a non-interest-bearing asset any increases in the price of gold must be driven solely by supply-demand mechanics, and among those who see gold moving higher, there’s one major demand source they point to that has yet to adapt to the environment of inflationary pressures and monetary debasement that have seen gold rise more than 100% over last two years.

That source is the $140 trillion in assets under management (AUM) controlled worldwide by institutional investors and fund managers, who in 2021 may have allocated a mere 0.5% to gold, and who even now seem to top out at 4%. Most funds and managers have a big fat 0% of their AUM allocated to gold.

The idea behind the gold price re-testing and breaking through its January highs of $5,600 again partly relies around the expectation that some of these fund managers, either in pensions, hedge funds, or family investment offices, move some of their capital to gold.

With $140 trillion managed, the percentage would only need to increase a little bit to see massive inflows into gold, particularly into gold-backed exchange-traded funds (ETFs), which stand as the preferred exposure method for institutions. An important 2021 study conducted by Australian researchers was the first to generate this estimation that gold holdings as a part of total worldwide AUM is around 1.7% on average, with 30% or fewer institutions having any allocation at all.

In October of 2025, as the price of gold had begun to go up virtually every day without fail, the Metals and Miners substack published a commentary of institutional gold holdings based on data obtained by Numera Analytics.

In light of Morgan Stanley’s revolutionary 60/20/20 portfolio allocation (20% gold) pronouncement, the massive debt pile growing exponentially from here, foreign nations slowly abandoning US Treasuries for gold, the largest central bank gold purchasing cycle in generations, and BRICS building a new gold settlement system to circumvent Western banking control, it’s clear that institutional investors controlling trillions in global wealth still have enormous gold buying ahead.

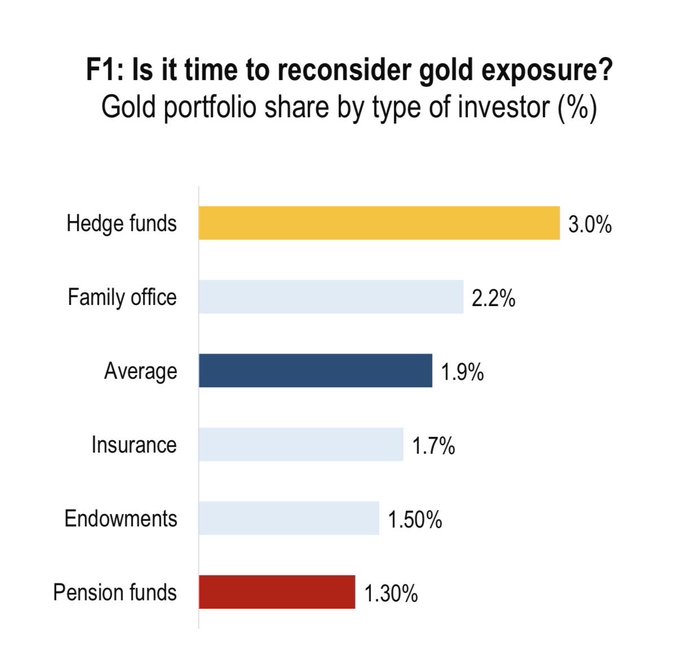

Numera’s data showed that among institutions that had any gold allocation, hedge funds maintained the highest weight of 3%, while pension funds maintained the lowest at 1.3%, despite controlling a total of $50 trillion.

On average, the of 1.9% of capital allocation to gold reflects just one-fifth of one-percent higher allocations than what were found in 2021 by the Australian researchers. In other words, over a period when the price of gold increased from $1,800 to $4,300 per ounce, total capital allocated to gold among all institutional investors remained virtually unchanged, even if perhaps it climbed among some, such as Morgan Stanley, and fell among others.

The shining implication

If any one of these institutional segments—hedge funds, family offices, endowments, pension funds, and insurance funds—brought their allocations up to just 5%, it would instantly create a bear minimum demand on the above-ground-gold market of $1 trillion. If just pension funds brought it up to 5% from 1.3%, it would create $2.5 trillion in demand.

Those are transformational, generational gains, and ones which could be reasonable to predict would hold for years. While gold has the potential to trade sideways for long periods, it never loses all the value it accumulates during a bull market. It has lost up to 50% of the gains it makes, but never all of it, and it always recovers.

Not long after the 1971 spike following the closing of the US gold window, when gold went from $41 an ounce to $200, it dropped down to $125, but never went below $100 again. 3 years later, it broke out beyond $200 and went to $640, and even though it dropped to hover around $400 for years, it never fell below $200 again. In 2007 it broke out beyond $650 and never even remotely looked back.

Another reason why it’s reasonable to suspect future increases would stick comes from a broad and detailed survey by the World Gold Council and Coalition Greenwich that included interviews with 400 decision makers and money managers at funds of all kinds worldwide.

Trends in institutional gold ownership were revealed, including that “the vast majority of gold allocations are strategic, typically held for more than three years,” and that “investors who own gold do so overwhelmingly for diversification and inflation-hedging purposes”.

Moreover, the interviews revealed that of those fund managers surveyed from North America, 7% responded that they did have specific gold allocations—less than half as much as their counterparts in the Asia-Pacific, or Euro-Mideast-Africa markets. That means of all the worldwide buying pressure, the North American market has the most room to run.

When the Australian researchers published their paper in 2021, the above-ground gold supply at then-current prices was around $12 trillion. In October of 2025, it stood at $27 trillion—a greater-than 100% move driven entirely off of central bank and retail investor buying.

Only when this institutional component of worldwide investment finance makes its move into gold—virtually an inevitability considering current inflation levels and everything else elaborated by Metals and Mining—can gold analysts finally have their theses and price targets tested.

Until then, gold has given all the gains it made between October and January’s high. The price seems to be testing support at $4,500 an ounce, pushed down by vague hopes of lower oil prices and a worldwide route in bonds that sent yields in various countries to multi-year, sometimes multi-decade highs.

Investors may consider it a good buying opportunity; certainly many gold media outlets are calling it just that. With the lack of North American gold allocation, US citizens may consider it an even better opportunity than those of other continents.

Editor’s Note: WaL maintains an affiliate partnership with renowned physical precious metals dealer and gold-IRA experts Lear Capital, which after $3 billion in bullion transactions and thousands of 5-star reviews on Trust Pilot have become a national leader in US gold investing. They are the bullion dealer of choice for thousands of Americans, including conservative-libertarian Judge Andrew Napolitano, and also manage gold-backed IRAs for those looking to back their retirement up with the best performing asset class over the last 50 years.