Earlier, WaL reported that, for the first time in 5 years, tin (Sn) is predicted to enter a supply deficit this year, joining other key base and precious metals like copper, silver, tungsten, platinum, and cobalt as factors of production where global demand outweighs finished product.

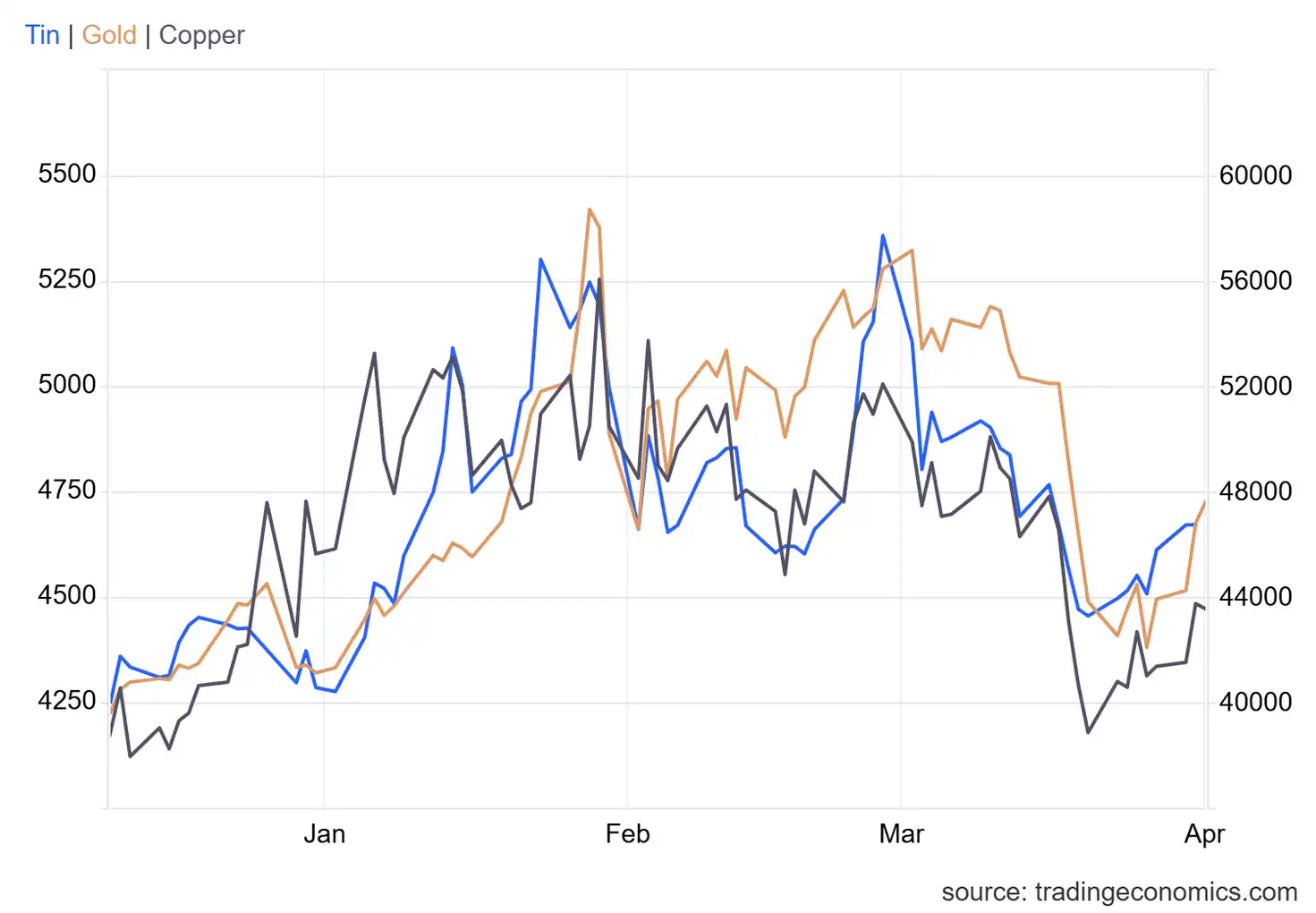

From the new year, tin prices climbed non-stop from $40,600 to $56,000 by January 19th, a 27.5% move up, and a high that it would eventually break a month later on February 23rd when it topped $57,000. Tin then followed the metals down sharply after the US and Israel launched their aggressive war against Iran.

With few exceptions, tin is trading in concert with gold and other metals like copper, but, in contrast to the latter metals, a lack of large cap Western supplies makes the trade a more volatile one, with sharper highs and steeper bottoms.

Though the US is heavily dependent on China for finished copper, buyers have multiple material sources across North and South America. Copper has made headlines across the investing world for the enormous supply deficits predicted for the next decade, with this year’s estimated to be 330,000 tonnes of finished metal.

However, though JP Morgan has a copper outlook, it hasn’t produced a case for tin. In fact, across the whole metals/commodity complex, tin is routinely left out, despite being the principal source of the world’s solder, and therefore a nearly-irreplaceable component of electronics manufacturing. Indeed, with the national industry focused on technology above all else, the United States is the world’s largest consumer, ex-China, of tin.

Just as with copper, South America along the Bolivian Tin Belt was a large tin producer in the 20th century, and the strategic tin reserve owned by the Pentagon, which once weighed in at 200,000 tonnes, was all mined in Bolivia.

Very much unloved compared to cobalt, copper, silver, and other industrial metals, the Pentagon routinely drew down its supply without replenishing it over the years, and allowed “tin pest” to erode around 20% of the total stockpile weight to away into dust. There is now just 1,978 tonnes of tin out of that 200,000 accumulated between 1939 and 1990. This neglect mirrors the neglect of tin in investment firms and financial markets.

Yet again, the direct parallel is copper, in that the US and much of the world besides allowed China to become the world’s leading tin producer and finisher, with two of the largest tin producers on Earth found in the country which produces over 50% of the world’s finished tin concentrate.

Where’s the next source?

The predicted supply deficit of tin, measured by credit risk management group Coface, is estimated to be 0.5% this year—a small decline that could be offset if new sources come online. There are so few new tin projects that each one has to open and perform to nameplate capacity for worse shortages to be avoided.

The Bisie Tin project in DR Congo operated by Alphamin Resources is one of these that must sustain current production for this end, but problems with armed insurgents have seen operations interrupted. Additional headwinds for tin came in Myanmar, a country containing a huge portion of known tin reserves, where the massive Man Waw mining complex in the northern Wa state has been out of action since June 2023.

In order to restart operations, significant dewatering of the underground mine’s lower levels needs to be carried out. The International Tin Association (ITA) reported in early March that Wa State Industrial and Mineral Resources Management Bureau (IMRB) released a document formalizing the process for sharing pumping costs across 11 mine portals. Operators would receive a 5% royalty on sold concentrate to cover the dewatering which is split across a number of firms currently preparing to restart the giant mining complex.

Atlantic Tin’s Achmmach project in Morocco, containing over 200,000 tonnes tin was mostly bought out by Xingye Silver and Tin, which run a very large tin mine in Inner Mongolia, but which is listed on the Shenzhen Stock Exchange which American brokers cannot trade on. At the time, the ITA noted how greatly this consolidated future tin production into China’s sphere, as Achmmach was “one of the most promising new supply projects,” anywhere in the world.

Chinese consolidation was also seen in the restart of the Renison Bell Mine in Tasmania, where a 50-50 joint venture with Australian miner Metals X and a subsidiary of Yunnan Tin, the world’s largest tin producer and finisher, got a 200,000-plus tonne deposit back into production.

Major sources may be found in Bolivia. In March, WaL reported that Eloro Resources published a maiden resource estimate on their land package showing around 133,000 tonnes of tin juxtaposed with a high-grade polymetallic Ag-Zn-Pb (silver-zinc-lead) project. While this wouldn’t be a Tier 1 tin asset, it and the company looking to develop it, would be readily accessible for Western investors.

Beyond that, recent research (from China, albeit) has pioneered a new magnetic-based recovery method of tin from mine tailings. More and more, companies are using old mine tailings that were milled during periods when metallurgical recovery of all minerals was poorer, as new sources of reserves. DRDGold in South Africa has built a 2.5 billion market-cap off of producing gold exclusively from mine waste.

Tin is primarily mined from the mineral cassiterite, a brittle material that can easily be pulverized in conventional mining ore crushers to a fine power too small to extract tin from. Developed by scientists at the Kunming University Land Resource Engineering faculty, centrifugal-magnetic separation of a pre-concentration tailings sample recovered 89.5% tin. That sample was then subjected to a process of volatilization through magnetic roasting and magnetic separation, which recorded a comprehensive tin recovery of 81% by the end of the process.

This could yield some added tin supply without the long process of exploration, development, permitting, and construction that is required to build a mine, but only if the US or US companies could find tailings dumps to process. However, no major source of tin ore was ever discovered in the country, so the tailings would have to be found elsewhere.

Unless major exploration is undertaken, and/or the security and political situation in Wa State and North Kivu in DR Congo substantially improve, predicted tin deficits will increase. WaL

We Humbly Ask For Your Support—Follow the link here to see all the ways, monetary and non-monetary.

PICTURED ABOVE: The Achmmach Project site in Morocco, one of the largest sources of tin to come online in the next 5 years. PC: Atlantic Tin.